The reforms to IR35, enacted in April 2021, resulted in new legislation referred to as off-payroll working, which applies where contractors work for medium to large companies. This guide explains the key terms within the legislation concerning the supply-chain and where the tax risk sits.

Off-payroll & IR35 – same, but different

IR35 is a non-statutory colloquial term used to describe two sets of tax legislation designed to combat tax avoidance where workers are supplying their services to clients via an intermediary, such as a limited company, but who would be considered an employee if the intermediary was removed.

The original IR35 is the Intermediaries Legislation (Chapter 8 of ITEPA 2003) enacted in 2000, which now only applies to workers working for small firms (see small companies exemption). The new legislation is the off-payroll working legislation (Chapter 10 of ITEPA 2003), which rolled out to the private sector in April 2021.

There are considerable differences between the original legislation and the new legislation. However, the common theme is the concept of a “deemed employee” and ascertaining whether tax implications must be followed.

If the original legislation applies (where the contractor is engaged by a small business), then the worker is responsible for assessing whether they are “Inside IR35” (rules apply) or whether they are “Outside IR35” (rules do not apply) and then paying the appropriate extra taxes if necessary.

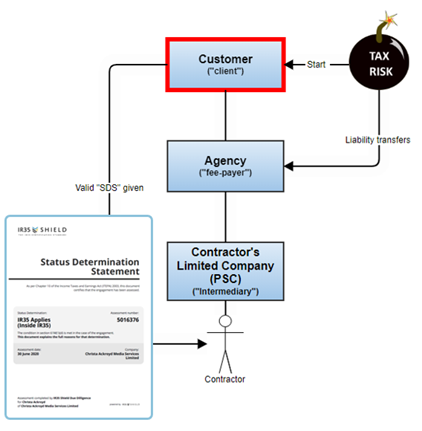

Under the newer off-payroll legislation, where the client is a medium or large sized business, the “client” should consider whether the relationship is “deemed employment” and the “deemed employer” is required to pay the taxes – but who are these parties in the supply chain?

Off-payroll & IR35 – the key terms

The critical terms contained within the legislation to understand are:

- Client

- Fee-payer

- Deemed Employer

- Intermediary

- Worker

The parties then fit into the supply chain, as defined within the legislation.

Off-payroll & IR35 – who is the “worker” and the “client”?

Section 61M(1)(a) tells us who “the worker” and “the client” are:

-

61M Engagements to which Chapter applies

- Sections 61N to 61R apply where—

- an individual (“the worker”) personally performs, or is under an obligation personally to perform, services for another person (“the client”),

We, therefore, know that the “client” is the hiring firm for whom the personal work is being provided.

The “worker” is the contractor, who will be working via their limited company, sometimes referred to as a Personal Service Company (PSC), a colloquial term to describe a one-person incorporated business.

Off-payroll & IR35 –what is the “chain”?

Section 61N(1) tells us what the “chain” is:

-

61N Worker treated as receiving earnings from employment

- If one of Conditions A to C is met, identify the chain of two or more persons where—

- the highest person in the chain is the client,

- the lowest person in the chain is the intermediary, and

- each person in the chain above the lowest makes a chain payment to the person immediately below them in the chain.

The conditions A to C essentially tell us whether there is a PSC in the supply chain which needs to be considered.

From the definitions, we know the “client” is the one at the top, and the bottom one is the intermediary, via which the worker provides their services personally.

Section 61N(2) also tells us that the party above the "lowest", which means the one above the intermediary, is the “fee-payer”. For example, if there is an agency in the chain, the agency would be the “fee-payer.” Otherwise the “client” and the “fee-payer” are the same party.

Off-payroll & IR35 – who and what is the “deemed employer”?

If the arrangement is assessed as one where the worker is a deemed employee, often referred to as “Inside IR35”, taxes need to be deducted and paid to HMRC, with the PSC receiving an amount net of taxes paid.

The party that must pay the taxes is called the “deemed employer”, and the "deemed employer" then pays the intermediary an amount of money referred to as the "chain payment". When that gets paid, and is treated as employment income, it is referred to as the "deemed direct payment."

The deemed employer could either be the “client” or the “fee-payer”, depending on whether a Status Determination Statement (SDS) has been given by the client to the worker prior to the payment being made.

-

61N Worker treated as receiving earnings from employment

- ...

- In this section and sections 61O to 61S—

“chain payment” means a payment, or money’s worth or any other benefit, that can reasonably be taken to be for the worker’s services to the client,

“make”—- in relation to a chain payment that is money’s worth, means transfer, and

- in relation to a chain payment that is a benefit other than a payment or money’s worth, means provide, and

“the fee-payer” means the person in the chain immediately above the lowest.

Off-payroll & IR35 – how can the deemed employer switch from the “fee-payer” to the “client”?

The “deemed employer” would normally be the “fee-payer”, but it can switch back to being the client if a Status Determination Statement (SDS) has not been given by the client to the worker and the fee-payer prior to the payment being made.

Section 61N(5) tells us that:

- Unless and until the client gives a status determination statement to the worker (see section 61NA), subsections (3) and (4) have effect as if for any reference to the fee-payer there were substituted a reference to the client; but this is subject to sections 61V and 61WA

Subsections (3) and (4) are about the necessity to pay the taxes by treating the payment made (“deemed direct payment”) as employment income.

If the determination is “Inside IR35”, where taxes need to be paid, the deemed employer must pay the taxes, and if they don’t, the tax risk sits with them.

Where there is no agency in the chain, then the client is the deemed employer and always holds the tax risk. Where there is an agency on the chain and an SDS has been given to the worker by the client, and to the agency (See 6N(5)-(8)), then the agency is liable to pay the taxes.

Off-payroll & IR35 – what is a Status Determination Statement (SDS)?

A ‘Status Determination Statement’ (SDS) is a comprehensive statement from the client which:

- Declares a contractor’s deemed employment status following an IR35 determination

- Provides reasons for reaching the status conclusion.

- The client took ‘reasonable care’ in arriving at its decision

This legislative requirement for an SDS was introduced in April 2021 and is intended to help combat misclassification of status due to non-compliant blanket or role-based assessments.

Despite a common misconception, no legislative requirement says an SDS must be produced or passed down – but failure to do so results in the consequences outlined in 61N(5)-(8), where the deemed employer can switch back to the client.

For a belt-and-braces compliance approach, IR35 Shield recommends that assessments and Statement Determination Statements are used in all cases and shared with the next party in the supply chain and the worker.

Key takeaways

Main points for all parties:

- Make sure you understand which party is the “client” and which is the “fee-payer” in your chain.

- The “deemed employer” is either the “client” or “fee-payer” and can change, depending on whether a Status Determination Statement (SDS) is created and/or whether it is given to the worker.

- A "statement" might not always qualify as an actual SDS.

Whether you are a contractor or a client, choose an expert partner to help manage your assessment process.